Unveiling 2024: Market Outlook and Key Trends Get your free copy

-

UK

- Australia - English

- België - Nederlands

- Belgique - Français

- Brazil - Portuguese

- Canada - English

- Česká Republika - Čeština

- Deutschland - Deutsch

- España - Español

- France - Français

- Ελλάδα - Ελληνικά

- Hong Kong - English

- Hong Kong - Traditional Chinese

- Italia - Italiano

- Luxembourg - English

- Nederland - Nederlands

- Polska - Polski

- Portugal - Português

- România - Română

- Schweiz - Deutsch

- Suisse - Français

- Sverige - Svenska

- United Arab Emirates - English

-

United Kingdom - English

Contact our experts

Ebury London

100 Victoria Street

London

SW1E 5JL

+44 (0) 20 3872 6670

[email protected]

Ebury.com

Markets brace for major central bank announcements

- Go back to blog home

- Latest

8 October 2019

Senior Market Analyst at Ebury. Providing expert currency analysis so small and mid-sized businesses can effectively navigate international markets.

Attention in the currency markets this week will turn back to monetary policy, with a number of major announcements from both sides of the Atlantic under the microscope.

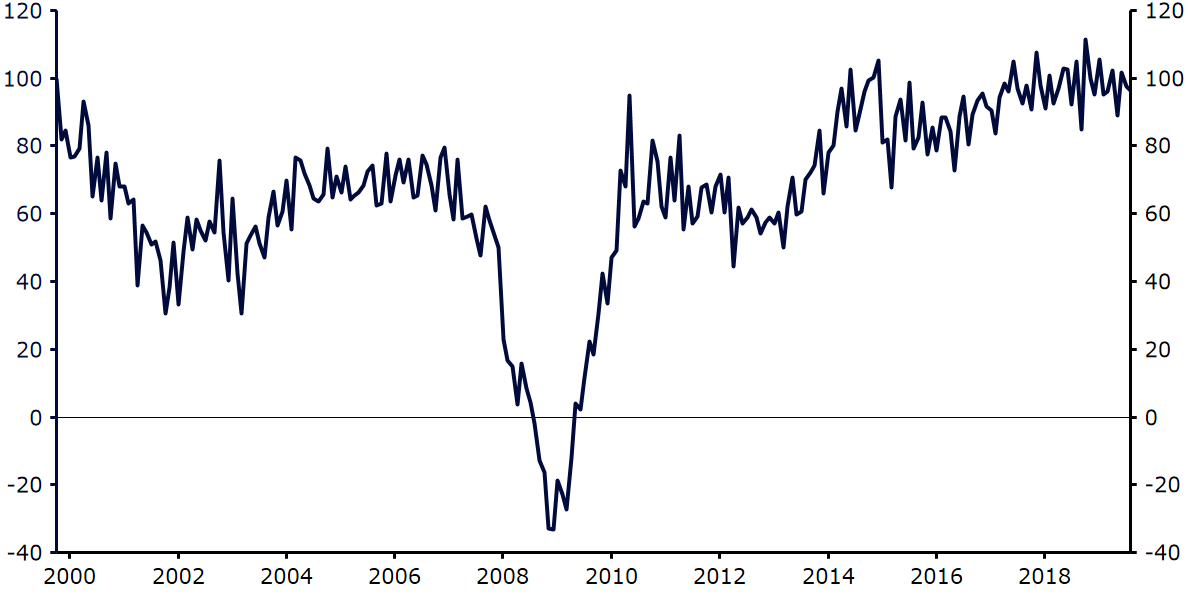

We have argued for a while, however, that macroeconomic conditions globally are not necessarily conducive of an aggressive pace of rate cuts. In order to convey this, we have constructed the below index that aims to give a broad gauge of macroeconomic conditions in both the US and the Euro Area. The index, which equally weights US nonfarm payrolls, the US ISM non-manufacturing PMI, German unemployment and Eurozone retail sales, has declined modestly since the beginning of the year, although has clearly not shown any signs whatsoever of trending towards recessionary levels.

Figure 1: Ebury’s US-EZ Economic Performance Index (1999 – 2019) [1999=100]

While these are largely lagging indicators that do not necessarily give the best idea regarding the possibility of a pending slowdown, they do show that economic conditions are currently holding up well, with much of the need for rate cuts instead driven largely by trade uncertainty.

In the markets on Monday, sterling fell to its lowest level in three weeks amid lingering concerns regarding a ‘no deal’ Brexit. While investors have grown increasingly confident that the Brexit deadline will be delayed, comments from Boris Johnson that the UK will leave the bloc come what may at the end of the month have got the market jittery. Meanwhile, EUR/USD continues to trade just below the 1.10 level, with investors awaiting news later in the week. Aside from monetary policy, trade talks will resume between the US and China. Any signs of progress will be good news for those higher risk currencies, with the New Zealand dollar already one of the better performing majors.

SHARE

Cookies and Privacy

This site uses cookies to ensure you get the best experience. For more information see our Privacy NoticeAccept Settings Reject

Privacy Overview

| Cookie | Duration | Description |

|---|---|---|

| cf_use_ob | past | This cookie is set by the provider Cloudflare content delivery network. This cookie is used for determining whether it should continue serving "Always Online" until the cookie expires. |

| cookielawinfo-checkbox-advertisement | 1 year | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Advertisement". |

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |

| Cookie | Duration | Description |

|---|---|---|

| _ga | 2 years | This cookie is installed by Google Analytics. The cookie is used to calculate visitor, session, campaign data and keep track of site usage for the site's analytics report. The cookies store information anonymously and assign a randomly generated number to identify unique visitors. |

| _ga_P8154YCRDP | 2 years | This cookie is installed by Google Analytics. |

| _gat_gtag_UA_51187572_50 | 1 minute | Google uses this cookie to distinguish users. |

| _gid | 1 day | This cookie is installed by Google Analytics. The cookie is used to store information of how visitors use a website and helps in creating an analytics report of how the website is doing. The data collected including the number visitors, the source where they have come from, and the pages visted in an anonymous form. |

| _hjFirstSeen | 30 minutes | This is set by Hotjar to identify a new user’s first session. It stores a true/false value, indicating whether this was the first time Hotjar saw this user. It is used by Recording filters to identify new user sessions. |

| _hjid | 1 year | This cookie is set by Hotjar. This cookie is set when the customer first lands on a page with the Hotjar script. It is used to persist the random user ID, unique to that site on the browser. This ensures that behavior in subsequent visits to the same site will be attributed to the same user ID. |

| CONSENT | 16 years 4 months 14 hours 27 minutes | These cookies are set via embedded youtube-videos. They register anonymous statistical data on for example how many times the video is displayed and what settings are used for playback.No sensitive data is collected unless you log in to your google account, in that case your choices are linked with your account, for example if you click “like” on a video. |

| pardot | past | The cookie is set when the visitor is logged in as a Pardot user. |

| Cookie | Duration | Description |

|---|---|---|

| IDE | 1 year 24 days | Used by Google DoubleClick and stores information about how the user uses the website and any other advertisement before visiting the website. This is used to present users with ads that are relevant to them according to the user profile. |

| test_cookie | 15 minutes | This cookie is set by doubleclick.net. The purpose of the cookie is to determine if the user's browser supports cookies. |

| VISITOR_INFO1_LIVE | 5 months 27 days | This cookie is set by Youtube. Used to track the information of the embedded YouTube videos on a website. |

| YSC | session | This cookies is set by Youtube and is used to track the views of embedded videos. |

| yt-remote-connected-devices | never | These cookies are set via embedded youtube-videos. |

| yt-remote-device-id | never | These cookies are set via embedded youtube-videos. |

| Cookie | Duration | Description |

|---|---|---|

| _lfa | 2 years | This cookie is set by the provider Leadfeeder. This cookie is used for identifying the IP address of devices visiting the website. The cookie collects information such as IP addresses, time spent on website and page requests for the visits.This collected information is used for retargeting of multiple users routing from the same IP address. |