Euro slides on recession fears, May secures modest A50 extension

- Go back to blog home

- Latest

25 March 2019

Chief Risk Officer at Ebury. Committed to mitigating FX risk through tailored strategies, detailed market insight, and FXFC forecasting for Bloomberg.

Last week proved to be a highly eventful one in the FX market.

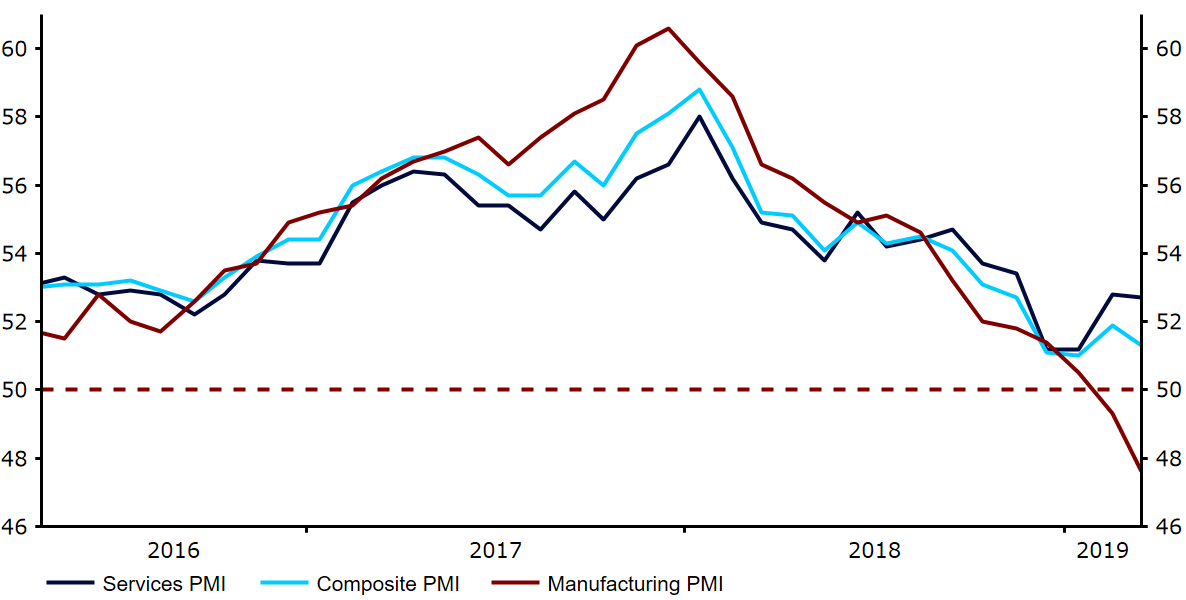

Figure 1: Eurozone PMIs (2016 – 2019)

In the UK, Theresa May was able to secure a modest extension to the Brexit deadline, albeit a shorter one than she had hoped for. Brexit will continue to dominate activity in the currency markets this week. May is expected to put her withdrawal agreement to a third vote in the House of Commons, possibly on Tuesday, although this is again looking very likely to fail.

GBP

Sterling continued to behave like an emerging market currency last week. Concerns over a ‘no deal’ Brexit sent the currency crashing on Thursday, although it did recover towards the end of the week after the EU granted to the UK a modest extension to Brexit.

The UK is now set to leave the EU on 22nd May, providing Theresa May forces her withdrawal agreement through a parliament vote. Should her deal again be rejected, the EU exit date will be pushed until 12th April and the government would need to request a longer delay or risk crashing out without a deal. In this event, we think we could well see the Pound head well below the 1.30 mark, as investors brace for the possibility that the UK leaves the EU in a little over two weeks time without a deal in place.

We do, however, still think that either an extended delay to the Brexit process or a negotiated deal are the most likely outcomes, which should keep the Pound trading above the 1.30 level.

EUR

Last week’s critical Eurozone PMIs were a massive disappointment, sending the Euro over half a percent lower against the US Dollar on Friday. While the services index has held up relatively well, manufacturing activity continues on its sharp downtrend. The index sank to just 47.6 in March, comfortably in contractionary territory. This was driven largely by an appalling performance of the German manufacturing sector.

Such soft data is a concerning development and reignites concerns that the Eurozone economy may be heading for a recession in 2019. In our view, it also puts yet another nail in the coffin for any faint hopes that the ECB could raise interest rates at some point later this year. This lack of policy action is, we believe, likely to keep the Euro around its currently suppressed levels this year.

USD

We had mentioned in our FOMC preview report that the key to the reaction in the USD was not whether the Fed would revise lower its rate hike projections, but by how much. This proved to be the case on Wednesday after the Fed’s latest ‘dot plot’ signalled that policymakers now do not expect to hike interest rates at all this year. This is a significant departure from the two pencilled in back in December and a more sizable downgrade than the market had anticipated.

Investors scrambled to price in rate cuts from the Fed over the next couple of years. We do, however, think this is somewhat of an overreaction and instead expect policy to merely be kept unchanged throughout the remainder of 2019. We reiterate that the current set up, combining low rates in the US with steady growth worldwide, is a very positive backdrop for emerging market currencies.

SHARE