Emerging market rally continues as investors chase yields

- Go back to blog home

- Latest

8 April 2019

Chief Risk Officer at Ebury. Committed to mitigating FX risk through tailored strategies, detailed market insight, and FXFC forecasting for Bloomberg.

As trade tensions between the US and China recede, and Chinese data improves, investors are feeling increasingly comfortable with the macroeconomic and policy backdrop worldwide.

This week, the ECB and the Federal Reserve will drive currency markets. The latter will publish the minutes from its last meeting, while the former will hold its April meeting. We expect both central banks to reiterate to markets their willingness to remain in a wait-and-see pattern for the foreseeable future.

Major currencies in detail

GBP

Theresa May tried to break the stalemate over Brexit by opening talks with opposition leader Jeremy Corbyn. As this is written, little progress seems to have been made, and a long extension or series of extensions to the Brexit deadline appears increasingly likely.

The two key factors driving Sterling this week will be the progress, or lack thereof, on the May-Corbyn talks and the EU Council meeting on Wednesday that is expected to rule on May’s request of an extension to Brexit to 30th June.

EUR

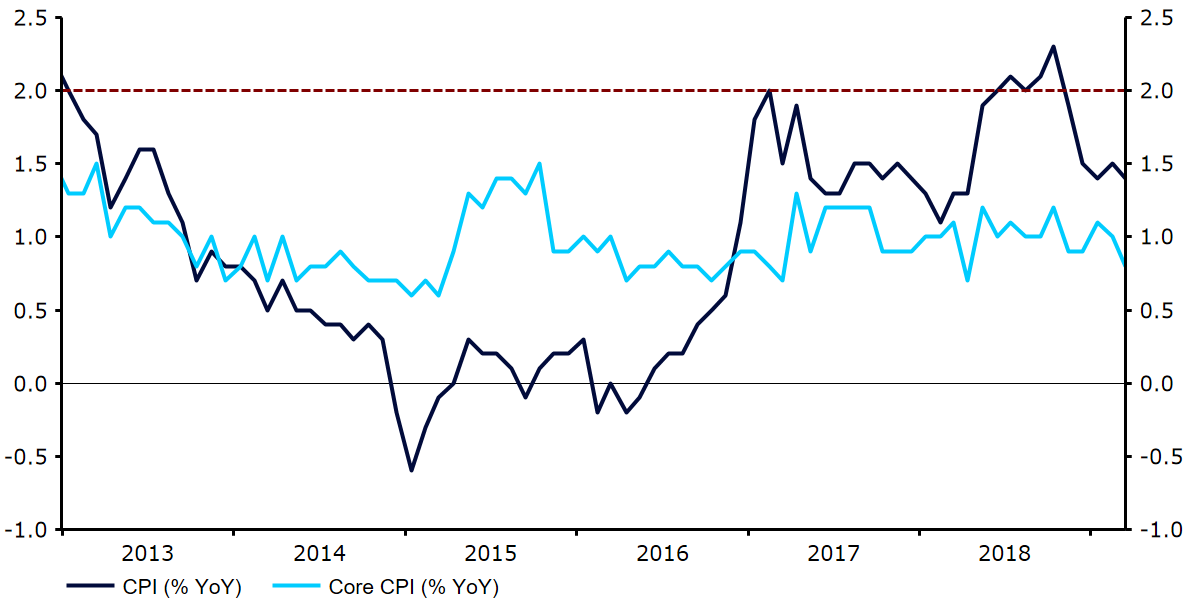

The ECB received some further bad news last week after the preliminary core inflation rate for March came in at a worse-than-expected 0.8% versus 0.9% that the market had priced in (Figure 1). This remains far from the institution’s target of “close to, but below 2%” and its lowest level in almost a year. Retail sales for February in the Eurozone rose 2.8% from the previous year. All in all, it seems likely that the economy will continue to post moderate gains for 2019, supported by the ECB’s monetary stimulus.

Figure 1: Eurozone Core Inflation (2013 – 2019)

We do not expect any monetary policy changes at the April meeting on Thursday, but there will be some lively discussion around the ECB’s option should it want to make policy even more stimulative, and the effect of negative rates on the banking system.

USD

Job creation in the US rebounded in March from the February dip. Labour data thus adds to the narrative that the slowdown seen in the early weeks of 2019 was a temporary phenomenon, likely driven at least in part by statistical quirks of seasonal adjustment in the first quarter.

In addition to the Fed minutes from the March meeting, inflation data out Wednesday will provide a test to the Federal Reserve’s new stance that it can be relaxed about inflationary pressures and hold rates unchanged for the remainder of 2019.

SHARE